How AI Electricity Demand Is Reshaping America's Utility Sector

By The Intelligence Edge Research Team · July 1, 2026 · 38 min read

AI data centers are driving the first surge in US power demand in 20 years. Who builds the electricity — and who profits — is the real question.

For two decades, the amount of electricity America used barely moved. Then the machines that run artificial intelligence arrived — and a power system built for a sleepy, predictable future is now the single biggest constraint on the most expensive building boom in corporate history.

- The flat line is broken. U.S. electricity demand grew about 0.1% a year from 2005 to 2019. It is now running near 2% and accelerating, with regulators forecasting a 24% jump in peak demand — roughly 224 gigawatts — over the next decade.

- Data centers are the engine. They consumed about 4.4% of U.S. power in 2023 and could reach 9% to 17% by 2030. In Virginia they already eat more than one kilowatt-hour in four.

- The bottleneck is not generation. It is the queue to connect, the transformers (now a 128-week wait) and the gas turbines (sold out through 2028). Steel and copper, not silicon, set the pace now.

- The money is staggering. The four biggest tech spenders are guiding to roughly $725 billion of capital spending in 2026, up from about $410 billion in 2025 — most of it AI data centers and the power to run them.

- The winners are unglamorous. Regulated utilities, the companies that make grid equipment, and the owners of existing nuclear plants are the clearest beneficiaries — while the bear case is not a bubble in power, but the bill landing on ordinary ratepayers.

On a humid morning in Ashburn, Virginia, traffic crawls past a row of windowless grey boxes the size of warehouses. There are no signs, no logos, almost no people. Inside, tens of thousands of processors hum through the calculations that answer your chatbot questions, rank your social feeds and train the next generation of artificial intelligence. This stretch of exurban Loudoun County is known in the industry as "Data Center Alley," and it is now the largest concentration of computing power on Earth. It is also, quietly, one of the largest single draws on an American electricity grid that — until very recently — nobody worried about at all.

For most of this century, the U.S. power business was the closest thing the stock market had to a sure, boring thing. Demand was flat. Utilities earned steady, regulated returns. Analysts could copy last year's forecast into this year's model and be roughly right. That world has ended. The arrival of generative AI has set off a capital-spending race among the world's richest companies, and that race runs on one input above all others: electricity. The story of who supplies that electricity — and who profits from supplying it — is the most important industrial narrative in American markets today. It is also widely misunderstood. This report lays out what is actually happening, what the numbers say, who stands to benefit, and where the thesis could break.

The End of the Flat-Line Era

To understand why investors are suddenly obsessed with power, start with a single, startling fact. Between 2005 and 2019, total U.S. electricity demand grew at an average rate of about 0.1% a year, according to the Energy Information Administration (EIA), the data arm of the federal government.2 Over that same period the U.S. economy more than doubled in size. Americans bought more gadgets, more screens and more air conditioning, yet the grid barely grew, because efficiency gains in lighting, appliances and industry quietly cancelled out the new demand. Electricity and economic growth had, in the jargon, "decoupled."1

That long truce is over. Since 2019, U.S. electricity demand has risen about 6%, from 3,813 terawatt-hours to 4,051 terawatt-hours in 2025, and the pace is quickening. The EIA now forecasts national electricity sales to top 4,230 terawatt-hours by 2027, roughly 10% above 2023 levels.1 A literature review from Columbia University's Center on Global Energy Policy found that utilities' own five-year load-growth forecasts, filed with the Federal Energy Regulatory Commission (FERC), nearly doubled in a single year — from 2.6% in 2022 to 4.7% in 2023.1

The grid's reliability watchdog has sounded the loudest alarm. In its 2025 Long-Term Reliability Assessment, the North American Electric Reliability Corporation (NERC) projected that summer peak demand across the bulk power system would grow by 224 gigawatts over the next ten years — a 24% increase from the 2025 peak, and more than 69% higher than the equivalent forecast just one year earlier. NERC was blunt about the cause: "New data centers account for most of the projected increase."3 To put 224 gigawatts in perspective, that is the equivalent of adding the entire peak power needs of well over a hundred million homes to a grid that is already straining in places.

The numbers behind that chart are the heart of the story. Data centers used roughly 58 terawatt-hours of electricity in 2014. By 2023, that had tripled to about 176 terawatt-hours — around 4.4% of all U.S. power — according to a Lawrence Berkeley National Laboratory study for the Department of Energy.4 Crucially, the annual growth rate jumped from about 7% before 2018 to roughly 18% after, as power-hungry AI hardware took over.5 Looking ahead, the Electric Power Research Institute (EPRI) projects data centers will consume between 9% and 17% of all U.S. electricity by 2030, up from 4% to 5% today. The spread between those scenarios — a low of 383 terawatt-hours and a high of 793 terawatt-hours by 2030 — is itself one of the central uncertainties of the entire investment case, and we will return to it.6

Why One Building Can Eat a City's Power

What makes an AI data center different from the data centers of the past — the ones that quietly hosted websites and email for two decades without troubling the grid — is density. A traditional server rack might draw 5 to 10 kilowatts. A rack packed with the graphics processors used to train AI models can draw 100 kilowatts or more, and runs flat out, 24 hours a day, every day. A single large AI campus can require one gigawatt of power or more — comparable to a major city, or to a full-size nuclear reactor — concentrated on one site, demanded all at once, and needed years before the grid can realistically build for it.

- Data center

- A building full of computer servers. AI data centers are far denser and more power-hungry than the web-hosting kind that came before.

- Hyperscaler

- The handful of giant cloud and AI companies — Amazon, Microsoft, Google (Alphabet) and Meta — that build data centers at vast scale.

- MW vs MWh

- A megawatt (MW) is a rate of power — how much is drawn at any instant. A megawatt-hour (MWh) is an amount of energy — a megawatt sustained for an hour. A gigawatt (GW) is 1,000 MW.

- Baseload

- Power that runs around the clock, regardless of weather or time of day. Nuclear and natural gas can provide it; solar and wind, on their own, cannot.

- Capacity factor

- How often a plant actually runs versus its theoretical maximum. Nuclear plants run above 90%; solar farms, around 25%.

- Interconnection queue

- The waiting line to plug a new power plant — or a new giant customer — into the grid. It can take years.

- PPA

- Power purchase agreement: a long-term contract to buy electricity at a set price, often used by tech firms to lock in supply.

- Rate base

- The total value of the poles, wires and plants a regulated utility is allowed to earn a guaranteed return on. Growing it is how these utilities grow profits.

That concentration is why a handful of regions — not the country as a whole — feel the strain first. Virginia is the extreme case: data centers there already consume more than 25% of the state's electricity, an estimated 32 of 128 terawatt-hours in 2023, and EPRI projects that share could climb to between 39% and 57% by 2030.7 No utility anywhere planned for a single customer class to swallow more than half a state's power in the span of a decade. The grid was simply never designed for loads that arrive this big, this fast, in this few places.

When power demand was flat and spread out, utilities could plan calmly. AI data centers flip that: they want enormous amounts of power, in specific places, on a timeline measured in months — while the grid is built on a timeline measured in years. That mismatch is the source of both the opportunity and the risk in every section that follows.

The Real Bottleneck Isn't Power Plants

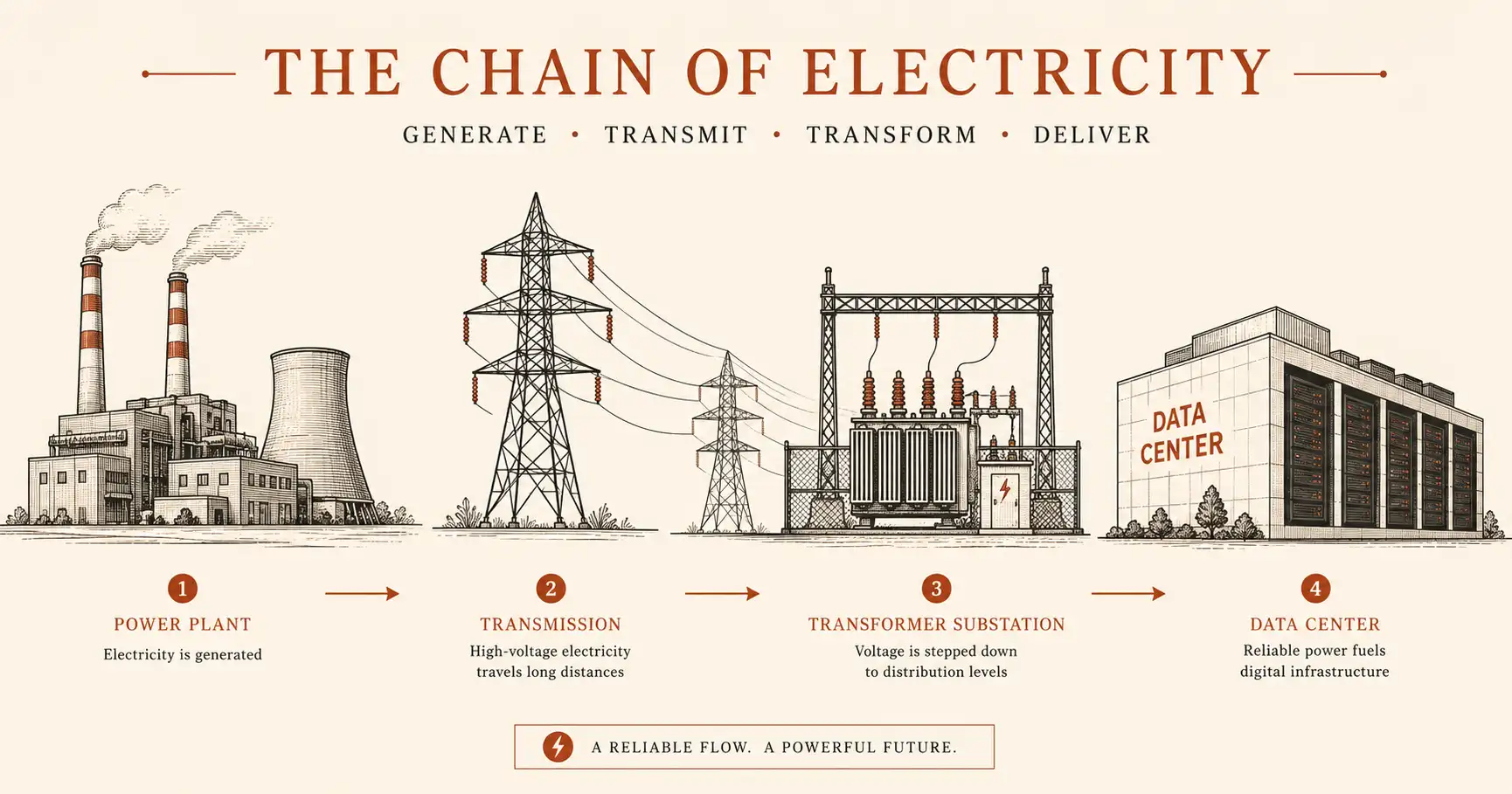

Here is the counterintuitive truth that separates a sophisticated read of this story from the headlines: the hardest part of powering AI is not generating the electricity. It is everything in between. You can announce a gigawatt of new gas plants tomorrow, but you cannot connect them — or the data center that needs them — without transformers, transmission lines, switchgear and a regulator's sign-off. Those are the choke points, and they are getting worse.

Consider the humble transformer, the unglamorous steel-and-copper box that steps voltage up and down so power can travel and be used. Lead times for standard power transformers have stretched to about 128 weeks — nearly two and a half years — according to industry trackers, with specialized large units quoted at 36 to 60 months.13 A piece of equipment that cost a few thousand dollars and shipped in twelve weeks before the pandemic is now a multi-year procurement saga. You cannot build a grid faster than you can build its transformers.

Then there is the queue. In Texas, grid operator ERCOT is staring at an interconnection request backlog that has ballooned past 400 gigawatts — multiples of the entire grid's current size — as developers rush to stake claims.14 FERC, the federal regulator, has been forced to act, ordering grid operators across six regions to revise the rules for how giant new loads like data centers get connected, precisely because the existing process was buckling.15 The agency has also repeatedly rejected attempts by data centers to plug directly into existing nuclear plants — most notably a proposed Amazon-Talen arrangement at the Susquehanna plant in Pennsylvania — on the grounds that such "behind-the-meter" deals could unfairly shift costs onto everyone else's electricity bills.8 The plumbing of the grid, in other words, has become a regulatory and political battleground.

Where the Electricity Will Actually Come From

If demand is real and the grid is the bottleneck, the obvious question is: what gets built to meet it? The honest answer is that the near-term and the long-term look completely different, and confusing the two is the most common mistake investors make.

In the immediate term, the grid is filling the gap with whatever can be built fastest. EIA data, compiled by the Carnegie Endowment, shows that of the capacity planned to come online in 2026, solar dominates at about 43 gigawatts, followed by battery storage at 24 gigawatts and wind at nearly 12 gigawatts. New natural gas? Just 6.3 gigawatts.8 That surprises people who assume gas is riding to the rescue. It is not — not yet — for a simple reason: you cannot get a turbine.

The longer-term picture reverses. Natural gas is where the structural buildout is heading: utility plans nationally now include 94 to 100 gigawatts of new gas through 2035, and globally the Brookings Institution estimates fossil fuels will supply about 64% of the incremental generation serving data centers between 2023 and 2035.89 The constraint is the machinery. GE Vernova, the dominant maker of heavy-duty gas turbines, has a backlog of roughly 100 gigawatts and is sold out of turbine deliveries through 2028, with only about 10 gigawatts of slots left across 2029 and 2030 combined.1011 Its rival Siemens Energy has commitments approaching 90 gigawatts. A new turbine order placed today carries a lead time of about three years.11 The bottleneck has simply moved from the power plant to the factory that builds the power plant.

| Source | Speed to deploy | Runs 24/7? | Near-term scale | The catch |

|---|---|---|---|---|

| Natural gas | Medium (turbine wait ~3 yrs) | Yes | Constrained by turbine supply | Emissions; fuel-price and pipeline risk |

| Nuclear (existing / restart / uprate) | Fast for restarts & uprates | Yes | Limited — few sites left | The best plants are already spoken for |

| Small modular reactors (SMRs) | Slow (first units 2028–2030+) | Yes | Negligible this decade | Unproven at commercial scale; delays common |

| Solar + battery storage | Fast (months to ~2 yrs) | No (hours of storage only) | Largest near-term additions | Intermittent; needs firm backup for 24/7 loads |

| Wind | Medium | No | Moderate | Intermittent; permitting and siting friction |

Gas vs Nuclear: The Defining Bet

No debate animates this sector more than gas versus nuclear. The short version: gas wins the rest of this decade on availability, and nuclear wins the structural, multi-decade story on round-the-clock, carbon-free reliability — which is exactly why the tech giants are signing nuclear deals years before they can use the power.

The nuclear land-grab has been remarkable. The pattern is unmistakable: the hyperscalers are paying a premium — estimated at $110 to $130 per megawatt-hour against wholesale prices of $50 to $60 — to lock up scarce, reliable, carbon-free baseload for decades.16 The headline deals:

- Constellation Energy & Microsoft — a 20-year deal to restart the undamaged Unit 1 reactor at Three Mile Island, the site of America's most infamous nuclear accident, rechristened the Crane Clean Energy Center, supplying about 835 megawatts.16

- Constellation & Meta — a separate 20-year agreement for about 1,121 megawatts that keeps the Clinton plant in Illinois from closing.8

- Vistra — roughly 2.6 gigawatts of deals with Meta and 1.2 gigawatts with Amazon (at Comanche Peak).16

- Talen Energy & Amazon — up to 1.9 gigawatts from the Susquehanna plant through 2042.8

- NextEra Energy & Google (Alphabet) — a power deal underpinning the restart of the Duane Arnold plant in Iowa (~615 megawatts).16

Gas is what actually gets built between now and 2030, because it is dispatchable and the technology is proven. The constraint is turbines, not gas itself. Owners of turbine manufacturing capacity and gas generation capture this window — provided supply chains and emissions politics cooperate.

Existing reactors, restarts and uprates are the scarcest asset in the system: carbon-free, round-the-clock, and impossible to replicate quickly. Small modular reactors are the long-dated call option — the global SMR pipeline reached about 47 gigawatts in early 2026 — but first commercial units realistically arrive 2028–2030, with broad availability not until the mid-2030s.

The Utilities in the Eye of the Storm

For all the excitement around AI chips, some of the most direct beneficiaries of this boom are the least glamorous companies imaginable: regulated electric utilities. To see why, you have to understand how they make money — and it is not the way most businesses do.

A regulated utility earns a guaranteed rate of return on its "rate base" — the value of the infrastructure it builds and operates. Build more poles, wires, substations and power plants to serve new demand, and — with the regulator's approval — the rate base grows, and so do earnings. For a utility, a wave of new data centers needing connection is, quite literally, a license to invest billions and earn a steady return on every dollar.

That mechanism explains the eye-watering capital plans utilities have unveiled. American Electric Power raised its five-year plan to $78 billion and now expects 63 gigawatts of new load by 2030, with 190 gigawatts sitting in its interconnection queue.17 Duke Energy lifted its plan to $103 billion.21 Southern Company, parent of Georgia Power, raised its spending to $81 billion against a 75-gigawatt large-load pipeline.18 Dominion Energy, the utility for Data Center Alley, plans roughly $65 billion through 2030 and has seen its pipeline of contracted data center capacity swell from 8 gigawatts in 2021 to about 70 gigawatts by early 2026.19

Then came the deal that reframed the entire sector. In May 2026, NextEra Energy — already America's largest utility by market value — announced an all-stock merger with Dominion worth roughly $67 billion. The combined company would serve 10 million customers across four states, command a combined large-load pipeline of more than 130 gigawatts, hold a $138 billion rate base, and target rate-base growth of about 11% a year through 2032.20 Analysts noted it could mark a return to the large, integrated utility model abandoned over the past decade — a model that may, ironically, be the best way to finance and execute infrastructure at the scale AI now demands.

| Company | Capital plan | Large-load pipeline | Flagship data center link |

|---|---|---|---|

| NextEra + Dominion (proposed merger) | $67B all-stock deal; $138B combined rate base | 130+ GW combined | $35B AWS investment across Virginia |

| Dominion Energy | ~$65B through 2030 | ~70 GW requested; ~48–51 GW contracting | Utility to "Data Center Alley," Virginia |

| NextEra Energy | $94B+ through 2030 | ~21 GW interest at FPL | Google PPA, Duane Arnold nuclear restart |

| Southern Co. / Georgia Power | $81B over five years | 75 GW; 10 GW contracted | $10B Compass campus (Mississippi Power) |

| American Electric Power | $78B (2026–2030) | 63 GW new load by 2030; 190 GW in queue | $33B Piketon, Ohio project (up to 10 GW) |

| Duke Energy | $103B (2026–2030) | +8 GW added in the Carolinas | $10B AWS campus, Richmond County, NC |

| Constellation Energy | $26.6B Calpine deal; 55 GW fleet | 10+ GW contracted clean deals | Microsoft (Three Mile Island), Meta (Clinton) |

| Talen Energy | — | — | Amazon, 1.9 GW from Susquehanna to 2042 |

| Vistra | — | — | Meta (2.6 GW), Amazon (1.2 GW, Comanche Peak) |

The Picks and Shovels: Beyond Utilities

In any gold rush, the reliable money is often made selling picks and shovels rather than panning for gold. The AI power boom has its own picks-and-shovels layer — the companies that make the scarce physical equipment every data center and every new power plant must have. Because their products are the bottleneck, their order books are arguably the cleanest read on the boom's real, funded demand.

GE Vernova has become the bellwether. Its gas-turbine backlog of roughly 100 gigawatts, sold out through 2028, is not a forecast — it is signed orders, with customers paying upfront to reserve slots.10 Siemens Energy reported total orders of about €17.7 billion in a single quarter, up nearly 30%, and raised its outlook on data center demand.12 Beyond the turbine makers sit the electrical-equipment specialists — companies like Eaton and Vertiv that supply the switchgear, power distribution and cooling systems inside the data center itself — and construction and transmission firms like Quanta Services that physically build the connections. When power equipment is the constraint, the firms that make it hold pricing power they have not enjoyed in a generation.

| Company | What they make | The signal |

|---|---|---|

| GE Vernova | Heavy-duty gas turbines, grid equipment | ~100 GW backlog; sold out through 2028 |

| Siemens Energy | Gas turbines, grid technology | ~90 GW commitments; orders +~30% YoY |

| Eaton | Electrical distribution, switchgear | Direct exposure to data center electrical fit-out |

| Vertiv | Data center power & cooling systems | Pure-play on rising rack power density |

| Quanta Services | Transmission & grid construction | Builds the connections utilities are funding |

Follow the Money: How the Hyperscalers Drive It All

None of this demand is hypothetical, and the proof is in the capital budgets of four companies. Amazon, Microsoft, Alphabet and Meta — the hyperscalers — have launched a spending cycle that dwarfs anything in technology history. In 2024 the four collectively spent over $200 billion on capital expenditure.4 For 2026 they are guiding to roughly $725 billion combined, the bulk of it AI data centers, chips and the power to run them — a 77% jump from about $410 billion in 2025.22 Goldman Sachs projects total hyperscaler capex from 2025 to 2027 will reach $1.15 trillion, more than double the prior three years.23

Why are all four spending at once, before the returns are proven? The simplest explanation is the right one: each fears being short on computing power more than it fears overspending. When Microsoft says it is "capacity constrained," it means its Azure cloud is turning away AI revenue it cannot serve — and lost demand compounds into lost market share. Microsoft has disclosed an $80 billion backlog of cloud orders it cannot fulfill because of power constraints.24 That single statistic captures the whole dynamic: the binding limit on the world's most valuable companies right now is not money, talent or chips. It is electricity.

Geography Is Destiny: The Regional Map

Because data centers cluster where land, power, climate and tax policy align, this is not a national story so much as a story about a handful of places. Where you sit on the map determines whether you are a winner, a battleground, or a cautionary tale.

| Region | Grid | The draw | Key data point |

|---|---|---|---|

| Northern Virginia | PJM | The world's largest data center market; fiber, land, history | 11,800 MW connected; 25%+ of state power |

| Texas | ERCOT | Cheap land, fast-moving (deregulated) grid, gas | 400+ GW interconnection queue; AEP Texas alone has 41 GW of load commitments |

| Ohio | PJM | Central location, incentives, available sites | $33B Piketon project, up to 10 GW |

| Georgia | Southern Co. | Pro-business policy, Southeast growth | ~8,500 MW of projected load growth by 2030 |

| Arizona | APS / regional | Land, solar resource, established tech presence | Active large-load rate cases underway |

The regional concentration matters for a reason beyond geography: it is where the political backlash is brewing. When one customer class drives up the cost of the entire local grid, ordinary households notice — and their elected officials respond. That brings us to the part of the story the bullish narratives tend to skip.

The Bear Case: Where the Thesis Could Break

"All I want to know is where I'm going to die, so I'll never go there." — Charlie Munger, on the discipline of inverting a problem: study how the thesis fails before you bet on how it wins.

Every compelling investment story attracts uncritical money, and this one is no exception. A serious investor should take the risks as seriously as the opportunity — so, in that spirit, here are the four ways this one could go wrong.

1. The demand might be overstated

The single biggest risk is that the headline forecasts are inflated. There is good evidence they might be. One analysis found utility and regional load forecasts could be overestimating data center growth by as much as 40%.30 The mechanism is mundane but powerful: developers engage in "queue shopping," filing multiple interconnection requests for the same project to find the fastest connection, and in "double counting," securing more sites as options than they ever intend to build. NERC itself flags this.3 A report commissioned by the Southern Environmental Law Center went further, calculating that meeting the projected 2030 demand from just 77% of the U.S. market would require 90% of the entire global supply of AI chips — a physical impossibility.31 Much of the "157 gigawatts" of announced capacity, in this view, is paper that will never be poured into concrete.

2. The circular financing problem

The capital fueling the boom increasingly flows in loops, and that worries some of the smartest people in finance. Nvidia agreed to invest up to $100 billion in OpenAI, which in turn buys Nvidia chips.25 Oracle signed a roughly $300 billion deal to supply computing power to OpenAI, much of which traces back to the same ecosystem. Microsoft and Nvidia put about $15 billion into Anthropic, which agreed to spend heavily on their cloud and chips; Amazon's investment in Anthropic reached $13 billion against Anthropic's commitment to spend $100 billion on AWS.26 Michael Burry, of "Big Short" fame, has likened Nvidia's practice of financing its own customers to the accounting that preceded the dot-com collapse.25 If the AI revenue underpinning these loops disappoints, the capital spending — and the power demand it implies — could retrench faster than any utility can re-plan.

3. The bill lands on ratepayers

The most immediate, concrete risk is political. In the PJM region — 13 states and 67 million people — the capacity auction that pays generators to be available cleared at $269.92 per megawatt-day for 2025–2026, an 833% jump in a single year, then hit the regulatory price cap of $329.17 for 2026–2027.28 The grid's independent market monitor attributed 63% of a 76% surge in wholesale prices to data center load, translating into roughly $9.3 billion in extra costs that ratepayers will absorb in a single year.29 Estimates put the average PJM household's bill increase at about $70 a month by 2028.28 The EIA projects that under a high-demand scenario, wholesale prices at the ERCOT North hub in Texas could be 79% higher by 2027.2 When voters see their power bills jump because of someone else's data center, legislators from Virginia to Oregon respond with rate reforms, special tariffs and even construction moratoriums — each of which can reshape the economics utilities are counting on.

4. Efficiency cuts both ways

Bulls and bears both invoke the Jevons paradox — the observation that making a resource more efficient to use can increase total consumption rather than reduce it. Alphabet says it cut the cost of serving its Gemini model by 78% in a year.22 Optimists read that as proof demand forecasts are too high; pessimists, and history, suggest cheaper AI simply means far more of it, pushing total power use up, not down. The uncomfortable truth is that nobody knows which force wins, and the answer swings the 2030 demand range by hundreds of terawatt-hours.

The contrarian case may be the most interesting of all: that the real danger is not too much power, but too little. Janus Henderson analysts argue the "overbuild" narrative confuses paper capacity with deliverable power — and that when physical constraints are applied, only about 85 gigawatts of the announced 157 gigawatts will realistically come online by 2030. If they are right, the binding risk for the decade is under-delivery, and the scarcest assets — turbines, transformers, existing nuclear — only grow more valuable.32

The Investor's Dashboard: Metrics That Matter

Because the central uncertainty is whether demand forecasts convert into built, paid-for infrastructure, the most useful thing an investor can do is watch the few indicators that reveal the truth in real time. These are the dials we will be tracking.

- Interconnection queues & signed contracts. Watch the gap between requested capacity and contracts with financial commitments behind them — that gap is the "phantom demand" filter.

- PJM and ERCOT capacity and wholesale prices. The clearest, fastest signal of real scarcity — and of mounting ratepayer pressure.

- Hyperscaler capex guidance. Each quarter's update from Amazon, Microsoft, Alphabet and Meta is the demand engine. Watch for any guide-down.

- Turbine and transformer lead times. When GE Vernova's backlog or transformer waits start shrinking, the bottleneck — and the pricing power — is easing.

- SMR milestones. Real licensing and construction progress (or slippage) at Kairos, Oklo, X-energy and TerraPower resets the long-term supply picture.

- Rate cases and state legislation. New special tariffs that ring-fence data center costs are good for utilities and ratepayers alike; moratoriums are a warning sign.

- NERC reserve margins. Falling reserve margins in PJM, ERCOT and MISO signal the system tightening toward the under-delivery scenario.

Final Investment Outlook

Strip away the hype and the doom, and a balanced picture emerges. The demand shock is real, the grid is genuinely constrained, and the companies that own scarce physical assets — reliable generation, the equipment to build it, and the regulated wires to deliver it — sit in an unusually strong position. But the headline forecasts are almost certainly too high, the capital fueling the boom is more circular and more fragile than it looks, and the political bill is only beginning to arrive. The most likely path is neither a clean boom nor a bust, but a messy, uneven, multi-year buildout in which execution — not ambition — decides the winners.

AI power demand grows strongly but below the most aggressive forecasts. Bottlenecks in turbines, transformers and interconnection persist, keeping pricing power with equipment makers and owners of existing generation. Regulated utilities compound rate base at high single-digit to low double-digit rates. Ratepayer backlash forces special tariffs that, on balance, protect both households and utility returns.

AI adoption keeps compounding, demand tracks the high scenario toward 17% of U.S. power, and under-delivery — not overbuild — defines the decade. Scarcity premiums widen across turbines, transformers and nuclear. The integrated-utility model, led by a NextEra-Dominion, proves the template for financing the buildout.

AI revenue disappoints, the circular-financing loops unwind, and hyperscalers cut capital spending. "Phantom" demand evaporates, leaving utilities and developers with stranded plans. The assets least exposed to speculative new-build — existing regulated wires and existing nuclear — hold up best; speculative merchant generation and richly-valued equipment names correct hardest.

For the new investor, the lesson is that the cleanest way to play a gold rush is rarely the gold itself — here, the AI chipmakers — but the scarce, unglamorous infrastructure everyone needs and nobody can build quickly. For the experienced investor, the discipline is to separate paper demand from deliverable power, to respect the political constraint, and to watch the dashboard above rather than the headlines. The electricity that powers artificial intelligence has become one of the defining industrial bottlenecks of the decade. The opportunity is real. So is the risk of believing every gigawatt that gets announced.

Frequently Asked Questions

Will AI really double data center electricity use?

Most credible forecasts point that way and beyond. U.S. data centers used about 176 terawatt-hours in 2023 (4.4% of national power) and EPRI projects 9% to 17% of U.S. electricity by 2030. The wide range — a low of 383 to a high of 793 terawatt-hours — reflects genuine uncertainty about how fast AI adoption and efficiency evolve.

Which companies benefit most from AI electricity demand?

Three groups stand out: regulated utilities that grow earnings by building infrastructure (such as NextEra, Dominion, Southern, AEP and Duke); equipment makers whose products are the bottleneck (GE Vernova, Siemens Energy, Eaton, Vertiv); and owners of existing nuclear generation signing long-term deals with tech firms (Constellation, Vistra, Talen). This is general information, not a recommendation to buy any specific stock.

Is natural gas or nuclear better positioned?

They serve different timeframes. Natural gas is what gets built this decade because it is dispatchable and proven — though turbines are sold out through 2028. Nuclear, especially existing plants and restarts, is the scarce, carbon-free, round-the-clock asset the tech giants are locking up for the 2030s. Small modular reactors are a longer-dated bet, with first commercial units realistically arriving around 2028–2030.

What is an interconnection queue?

It is the waiting line to connect a new power plant — or a large new customer like a data center — to the grid. Reviews and upgrades can take years, and the queues have grown enormous: Texas alone has more than 400 gigawatts of requests, far more than will ever be built.

Could AI efficiency reduce power demand instead?

It might slow it, but history suggests not reverse it. Under the Jevons paradox, cheaper and more efficient AI tends to be used far more, pushing total consumption up. Alphabet cut its Gemini serving costs 78% in a year — and still raised its capital spending sharply.

Why are my electricity bills going up because of data centers?

When utilities build new infrastructure to serve giant new loads, those costs can be spread across all customers. In the PJM region, capacity prices jumped more than 800% in a year, with the market monitor attributing most of a 76% wholesale price rise to data center demand — an estimated $9.3 billion passed to ratepayers in a single year. This is why many states are now creating special tariffs to make data centers pay their own way.

What is the biggest risk to the investment thesis?

That demand forecasts are overstated — possibly by 40% — because of double-counting and speculative interconnection requests. The opposing risk, argued by some analysts, is the reverse: that physical bottlenecks mean only about 85 of an announced 157 gigawatts gets built by 2030, making under-delivery, not overbuild, the real danger.

Public Companies Mentioned in This Article

For readers who want to dig deeper, here are the publicly traded companies referenced above, grouped by role, with live prices. Inclusion is for reference only and is not a recommendation to buy or sell any security.

Sources & References

- Center on Global Energy Policy, Columbia SIPA — "The Effects of Load Growth on Electricity Prices in the United States: A Literature Review." energypolicy.columbia.edu

- Utility Dive — "Data center demand spike could drive 79% ERCOT price hike in 2027: EIA" (citing U.S. Energy Information Administration data).

- Utility Dive — "NERC forecasts peak demand to rise 24% on new data center loads" (North American Electric Reliability Corporation, 2025 Long-Term Reliability Assessment).

- Belfer Center, Harvard Kennedy School — "AI, Data Centers, and the U.S. Electric Grid: A Watershed Moment" (citing Lawrence Berkeley National Laboratory). belfercenter.org

- EE Power — "Data Center Load Growth: What It Means for the Grid" (summarizing the LBNL / U.S. Department of Energy report). eepowerschool.com

- EPRI — "Powering Intelligence 2026," Executive Summary (data center share of U.S. electricity; low/medium/high 2030 scenarios).

- Electric Choice — "U.S. Data Center Power Consumption Map by State (2026)" (citing LBNL and EPRINC analysis for Virginia).

- Carnegie Endowment for International Peace — "Beyond the Hype: Assessing Hyperscaler Nuclear Commitments Against U.S. Energy Realities." carnegieendowment.org

- Brookings Institution — "Global energy demands within the AI regulatory landscape."

- Utility Dive — "GE Vernova gas turbine backlog hits 100 GW as prices rise."

- RTO Insider / Utility Dive — "Natural Gas Turbines Aren't 'Gating' Data Center Buildouts, GE Vernova Says."

- Siemens Energy AG — "Siemens Energy raises full-year outlook and releases preliminary results for Q2 FY 2026" (ad-hoc release).

- Industry procurement trackers — "Power Transformer Lead Times Hit 128 Weeks in 2026"; CWIEME Berlin, "24+ Month Lead Times: New Normal for Transformer Suppliers."

- Utility Dive — "Texas, facing 438 GW queue, approves initial large-load interconnection process" (ERCOT).

- White & Case LLP — "FERC orders grid operators to promptly revise or justify interconnection rules for data centers and large loads."

- Luminix — "Constellation Energy: Nuclear AI Power Deals & Market Position 2026." useluminix.com

- American Electric Power — "AEP Reports First-Quarter 2026 Earnings, Reaffirms Guidance." aep.com

- Utility Dive — "As load grows, Southern raises spending plan to $81B."

- Utility Dive — "Dominion Energy details its $65B, 5-year spending plan."

- Utility Dive — "Combined NextEra-Dominion would have 130-GW large-load pipeline."

- Stockopedia — "Duke Energy raises five-year capital expenditure plan to $103 billion as more US data centers sign on."

- Value Add VC — "~$725B AI Capex 2026: Microsoft vs Google vs Meta vs Amazon." valueaddvc.com

- Introl — "Hyperscaler CapEx Hits $600B in 2026: The AI Infrastructure Debt Wave" (citing Goldman Sachs 2025–2027 projection).

- Futurum Group — "AI Capex 2026: The $690B Infrastructure Sprint" (Microsoft Azure order backlog).

- Global Finance Magazine — "AI's Financial Circle Game." gfmag.com

- Built In — "How Circular Financing Is Fueling the AI Boom." builtin.com

- Introl — "PJM's $100 Billion Rate Shock: How Data Centers Are Rewriting America's Electricity Bills."

- Introl — "PJM's $100 Billion Rate Shock" (capacity auction clearing prices; household bill impact). See also ref 27.

- The AI Consulting Network — "PJM Power Prices Up 76% From Data Centers" (Monitoring Analytics; $9.3B ratepayer cost). theaiconsultingnetwork.com

- Shareholder proposal analysis — "Southern Co (SO): Report on Data Center Costs" (load forecasts potentially overstated by ~40%).

- Southern Environmental Law Center / London Economics International — "Overhyped data center growth is shaping our energy future" (chip-supply constraint on 2030 projections).

- Janus Henderson — "Data center power: Why the key risk is under-delivery, not overbuild." janushenderson.com

This article is for educational and informational purposes only and is not investment advice; do your own due diligence and consult a qualified financial advisor before making any investment decision.